Study warns PCR packaging growth falls behind PPWR 2030 targets

New research from Smithers, the global testing and market analyst, released its latest market study on post-consumer recycled (PCR) packaging, The Future of PCR Packaging to 2031.

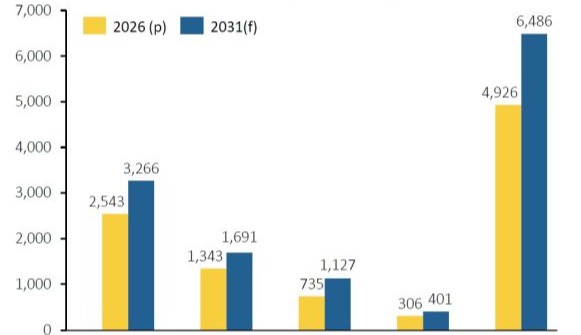

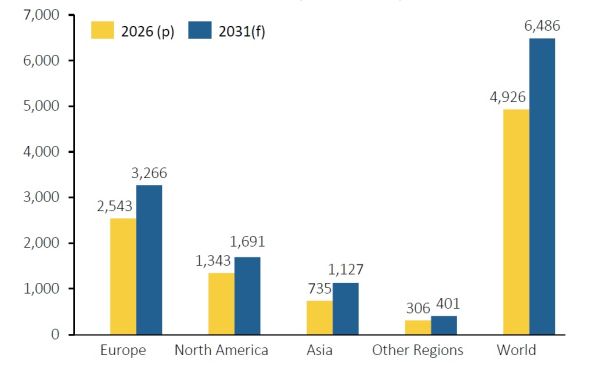

The global PCR packaging market sizes at 4.9 million tons in 2026. Smithers’ study forecasts to reach 6.5 million tons by 2031, with a compound annual growth rate (CAGR) of 5.7% over the 2026–2031 period.

PCR packaging consumption by region. (Source: Smithers)

Current PCR packaging landscape

rPET dominates the PCR packaging landscape, accounting for the largest volume share and projected to grow at the highest rate of 6.1% CAGR over the forecast period, driven primarily by beverage bottle applications. PE and PP follow as the next largest polymers by volume. PS, PVC and EPS are experiencing negative growth in many regions due to bans and restrictions on their manufacture and use.

By end-use, the drinks sector accounts for the largest share of PCR packaging consumption globally at 33.3%, followed by other consumer goods (26.7%) and food (19.1%).

Contamination and color requirements make food and drinks the most technically demanding applications, and therefore the sectors with most to gain from advances in sorting, decontamination and additive technologies.

Falling behind target despite growth and legislation framework

Europe remains the most established and fastest-growing market, driven by the Packaging and Packaging Waste Regulation (PPWR) and the Single-Use Plastics Directive (SUPD), which mandate significant PCR content in packaging by 2030.

Extended Producer Responsibility (EPR) frameworks in Asia and North America are also advancing, though with more limited success to date.

Despite these, the study warns that growth is falling short of what will be needed to meet legislated 2030 targets.

Obstacles: High cost and shortage of quality recyclate

The report identifies cost as the single biggest obstacle. rPET currently trades at approximately 35% above virgin polymer, a premium that many brand owners struggle to accept.

Compounding this are a global shortage of quality recyclate, contamination issues in food-contact applications, and a fragmented legislative landscape in which EPR rules vary across multiple levels of government.

Low-cost imported recyclate from Asia also threatens the viability of domestic recycling operations in Europe and North America. The European Commission has reported that growth in European plastics recycling capacity slowed from 17% in 2021 to just 6% in 2023, raising concerns about the closure of processing plants that cannot be replaced by imports alone.

How to accelerate PCR uptake

Smithers identifies several pathways to accelerating PCR uptake. Investment in mechanical recycling technology, including AI-driven sorting and robotics, is seen as critical. Robotics alone can increase clean rPET supply by up to 25% and reduce contamination by up to 60%. Closed-loop systems also offer significant gains in traceability and efficiency.

Chemical recycling is gaining ground as a complement to mechanical processes, particularly for hard-to-recycle materials such as flexible films and multi-layer packaging.

A February 2026 ruling by the European Commission now allows chemically recycled content to count toward PCR targets in PET single-use bottles, opening the door to broader commercialization, though the study notes it may take three or more years to translate into meaningful additional supply.

Other solutions highlighted in the report include the expansion of Deposit Return Systems (DRS) to improve recovery rates, eco-modulation frameworks that reward packaging carrying multiple sustainability attributes, and greater harmonization of EPR legislation to reduce compliance complexity.