What is delaying the recovery of the European chemical industry?

Chemical industry of the 27 countries in the European Union (EU27) continues to face a deep and structural competitiveness challenge, according to the Chemical Trends Report Q1 2026 of European Chemical Industry Council (Cefic).

Despite modest improvement in early 2026, weak demand, declining production and intensifying global competition persist, while increasing exposure to global trade risks, including US measures and geopolitical tensions affecting key routes such as the Strait of Hormuz, adds further uncertainty, with impacts still difficult to assess.

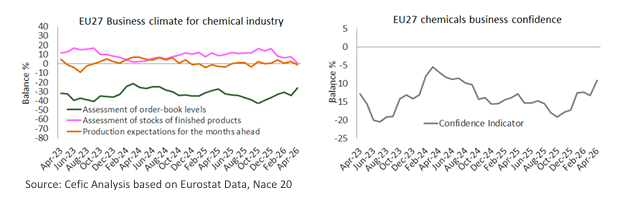

Confidence towards the market improves but remains negativity

Business sentiment shows early signs of improvement but remains fragile. Confidence has risen from -19% in October 2025 to -9% in April 2026.

However, it remains in negative digits, with firms remaining cautious about the sustainability of the current improvement phase. Demand conditions are still weak, with order books well below normal levels despite recent improvements.

Overall, the sector has moved from contraction to a fragile improvement rather than a firm recovery trajectory.

(Source: Chemical Trends report of Cefic)

Energy cost is still a challenge

A key structural constraint to European chemical industry competitiveness remains the persistent energy cost disadvantage faced by European chemical producers.

Although energy markets have stabilized since the 2022 crisis, European natural gas and electricity prices continue to exceed those in competing regions, particularly the US. In 2026 (Jan-Apr), gas prices in Europe remain 3.3 times higher than US levels, widening the transatlantic competitiveness gap compared with the pre-crisis period.

This enduring divergence continues to weigh heavily on energy intensive segments such as ‘other organic basic chemicals’, polymers and basic chemicals, constraining production, limiting investment and reinforcing the relocation pressures observed across global value chains.

Low capacity utilization and production trends

These pressures are reflected in persistently weak capacity utilization and declining production trends. EU27 chemical capacity utilization remains at historically low levels, around 74%, well below its long term average and consistently below overall EU manufacturing.

This underperformance confirms the structurally weaker position of chemicals within the European industrial base. In the first quarter of 2026, chemical production declined by 3.2% year on year, highlighting the fragility of the current trend. The downturn is particularly pronounced in “other organic basic chemicals” and polymers, while only selected specialty and consumer oriented segments show resilience.

Across Member States, the improvement remains highly uneven, with France showing modest growth, while Germany, Italy and the Netherlands continue to experience significant contractions.

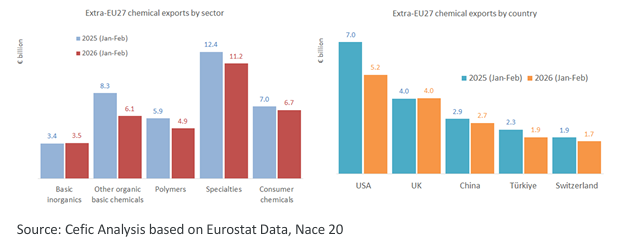

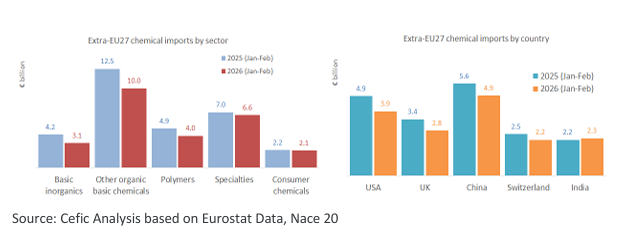

Weakened chemical trade, both exports and imports

EU27 chemical trade weakened markedly in early 2026, with exports falling by €4.6 billion (12.4%) and imports declining even more sharply by €4.8 billion (15.7%), reflecting both softer external demand and a contraction in domestic industrial activity.

The export downturn was largely driven by reduced shipments to key partners, particularly the United States, and by sharp declines in ‘other organic basic chemicals’, polymers, and other intermediate chemicals.

Imports showed a similarly broad-based decline across partners and sectors, again led by upstream segments, pointing to weaker demand for industrial inputs.

Despite these negative trends, the EU27 trade surplus increased slightly to €6.7bn, as the stronger fall in imports outweighed export losses. Overall, the improvement in the trade balance reflects import compression rather than a recovery in competitiveness, underlining a weak demand environment.

(Source: Chemical Trends report of Cefic)

EU27 chemical industry in fragile development

Overall, the EU27 chemical industry has entered a phase of fragile development rather than recovery. Without a sustained improvement in energy affordability, stronger demand conditions and a more stable global trade environment, the outlook remains subdued. The risk of a continued erosion of Europe’s chemical production base therefore remains significant in the medium term.